Can compound

interest provide a $1 million retirement?

Are you saving and

investing at least $250 a month in your retirement at work (401k, 403b) or IRA

on your own? Are you putting most of the money in low-cost stock mutual funds?

The other variable is time. Compound interest works when you have time on your

side. It takes about 33 years ($250 a month, $3,000 a year) with total

contributions of only $99,000 to reach $1,000,000. Even if you begin after age

30, you can still have much more than almost all your neighbors. According to

Warren Buffett, “My wealth has come from a combination of living in America

Forget

brokers/advisors: https://www.amazon.com/Warren-Buffetts-Investment-Secret-Steeple/dp/148418980

What about ETF up

35% this year?

What are the gurus

and TV marketing people so happy about? Your plain low-cost broad market index

that Buffett recommends is flat for 2018. So what can financial people talk

about? How about gold (JDST): Return year-to-date: 48.79%; One-month return:

28.66%. But after you look further, the three-year return is -77.62%. Natural gas?

(UGAZ): Return year-to-date: 51.62%; One-month return: 22.37%. But three-year

return: -51.43%. How about muni bonds (EVLMC)?: Return year-to-date: 100.76%; One-month

return: 0.11%. No track record for a three-year return: N/A. So what about

Treasuries (DLBS)?: Return year-to-date: 37.96%; One-month return: -0.74%. Not

much better than your bank savings account in three-year return: 0.24%. 500

Index (VFIAX)?: Return YTD: 3.83%; 5 year: 11.3%; 10 year: 13.22%. Salespeople

always have ‘shiny

objects’.

Buffett still has

the edge: https://www.amazon.com/Warren-Buffetts-Vanguard-Funds-Retirement/dp/1496148592

Do you need a REAL

middle-income tax break?

The REAL tax break

from the GOP and Trump is the removal of the income

cap on conversions from traditional IRAs to Roth IRAs. The 1.6% income

increase for the average household earning $50,000 to $75,000 has been eaten up

by tariffs and health care costs. Compare the $thousands you save in taxes

during retirement when most of your income is tax-FREE and you no longer have

to take taxable RMDs from your IRAs. For many, the elimination of tax on IRA

distributions means their income can continue to grow after 70 ½ AND they will

pay less tax or nothing on their SS

benefits.

Keep your taxes low

for life: https://www.amazon.com/Tax-FREE-Retirement-code-lifetime-income/dp/1475206976

Health ins plan scams

prey on the most vulnerable

“You can now get a

great insurance plan at the price you can afford. We make it hassle free to

sign up with the policies from Signa Blue Cross Etna United and many more.

Press one now to get a hassle free assessment or press two to be placed on our

do not call list. Thank you and it’s always be happy blessed.” Criminals

promise inexpensive health care plans and take personal information that’s used

to commit identity theft. In another version, victims are sold useless

healthcare discount plans that scammers frame as cheaper than the consumers’

current health insurance. A Florida-based company named Simple Health Plans

allegedly collected $100 million from tens of thousands of victims, Federal

Trade Commission lawsuit. Consumers paid up to $500 a month for

a relatively worthless product, the agency said.

It is easy to be

fooled: https://www.amazon.com/Health-Insurance-ONLY-right-policy/dp/1480125083

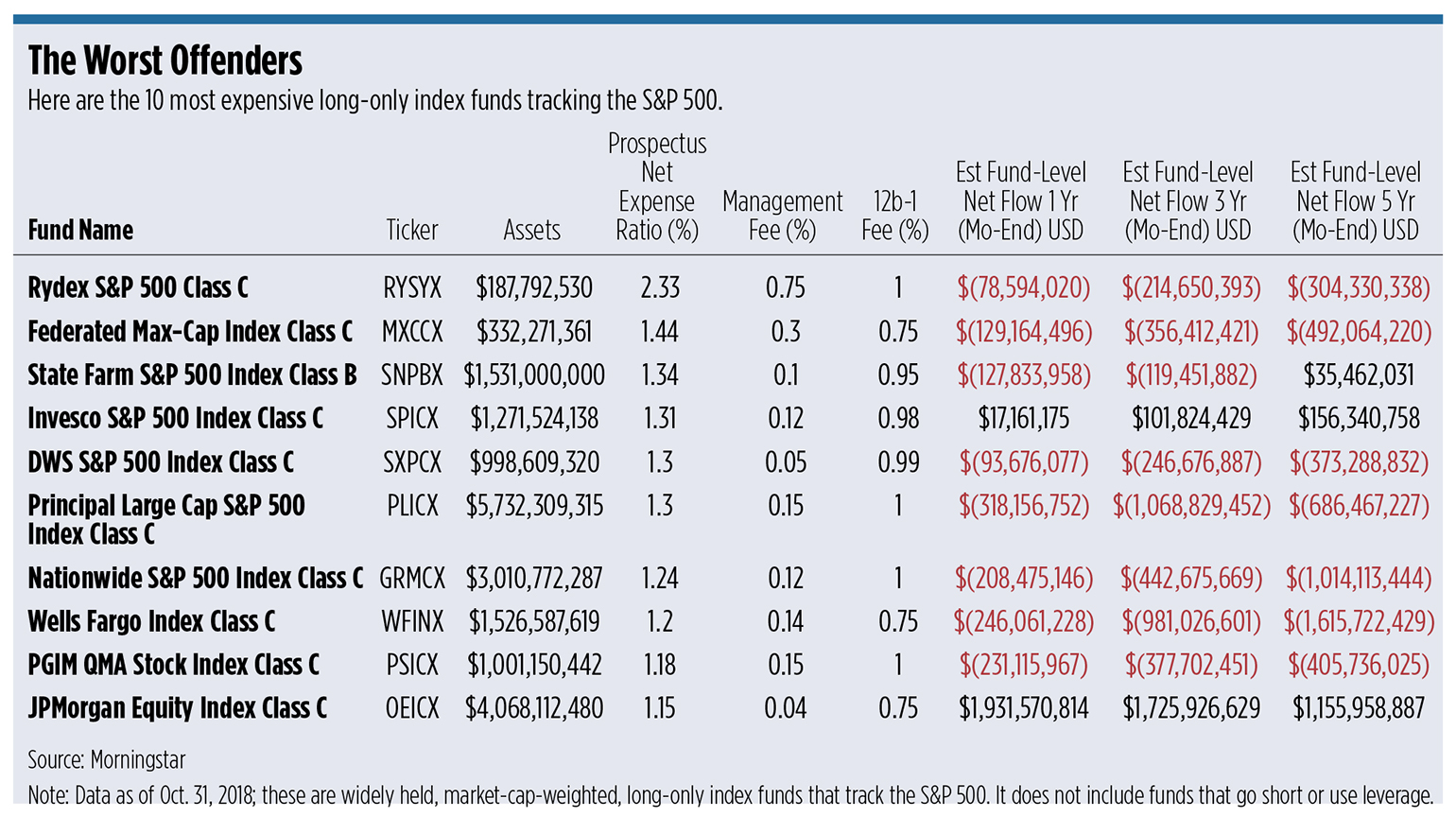

Do you own the

absolute WORST funds?

Why do people pay much

more for exactly the same commodities as others? Convenience? Inertia? B.S.?

Misleading benefits? Some advisors are charging 2.33% for the same product as

others charge 0.00%. Is that a ‘loss leader’? Sellers

need to make something in order to compensate for time spent on other

services they say. State Farm charges 1.34% for their plain 500 index fund. Do

their customers believe they are buying an insurance product? Many

insurers seem to be enjoying this extra profit. Perhaps customers are

finally getting the message—net flows are negative for 3 and 5 years. Customers

who feel more informed have chosen to separate financial providers/vendors.

Vanguard, not brokers, offered the index in 1976 for less. It is now the

largest mutual fund firm for a reason—costs matter. 11%

vs 3.79% return on your money is huge.

Go with the pro: https://www.amazon.com/Vanguards-Top-Ten-mutual-funds/dp/150073909X

Another way the ‘Tax

Credit’ class avoids paying their fair share

The IRS just

issued proposed regulations stating that there will be no clawback of

the use of any unified credit (gift tax exemption) before 2026 when the

lifetime exemption will revert from $10 million to $5 million. Wealthy

taxpayers may safely use the current $5+ million excess and, if death

occurs after 2025, still have $5 million for estate tax purposes, thanks to the

millionaire Congress. Similarly, a taxpayer could make a taxable gift now of

$11.18 million without concern that there would be a phantom estate tax on their

death after 2025. Passing on $11.18 million tax-free allows the kids to get the

‘head start they really need’? to create their own tax-advantaged business.

Use your tax credits

too: https://www.amazon.com/Tax-Credit-Class-your-credits-ZERO/dp/1539462382

****************

Two Americas

***********************

How Govt wastes our money: Congress spends $1.3 Trillion we don’t have!

Trump’s

stunt over: 5,800 troops not home for Thanksgiving. Cost us $220

million.

SCAMS/SPINS:

RoboCallers index:

Top 100 callers by volume https://robocallindex.com/top-robocallers

Health ins plan

scam: Simple

Health Plans FL promised one of Trump’s

‘great’ plans.

Hackers control your

pacemaker? Any

electronic implant can be controlled by others.

First Choice

Healthcare Solutions caught

‘pump and dump’ stock scam: $12.5 mil lost.

Elite Stock Research

caught

‘pump and dump’ stock scam: $10. mil lost.

Giga Entertainment caught

paying others to pump up sales software on Apple Store.

Check food: banned

flavors--methyl eugenol, benzophenone, ethyl acrylate and pyridine.

Ford’s robot

cars: “When we take the road, we know what doing and where

the profit is.”

Trump attacks

another distinguished patriot: draft

dodger says he could have done better.

Cheryl Ann Stallings

caught

controlling client bank accounts for profit

Scott Newsholme, FL

caught stealing

$3.1 million by various fraud: jail 8.5 years

Waddell Reed caught loading

its 401(k) plan with costly in-house investments. Fine only

H. Beck MD caught allowing

sale of unsuitable L-share variable annuities/riders. No jail.

Trump’s

mob using private email accounts too—lock them up too? “ijkfamily.com”

Trump

ordered Justice to prosecute 2 rivals just like tin dictator—McGahn said

“no”

The Don SAYS HE'S

MOST THANKFUL FOR HIMSELF ON THANKSGIVING

Is

there really a ‘master race’ in Kansas? Dorothy found out our

Wizards are frauds!

IRS audit? agents

for criminal investigations dropped below 2,100—Lowest since ‘60s.

----------------------------------

The Mob Boss can never go to jail: Trump

has Kava as Supreme so no indictment.

‘No man is above the

law’ … well up till now. Dictators

nullify courts first, then votes.

Supremes protect

Don’s ‘Orders’? – GOP: Sure, pres

can change

Constitution anytime.

----------------------------------

Jobs:

Who owns your account now?

Avoid

mistakes like these in passing on your accounts and assets.

Need your IRS tax file?

https://www.irs.gov/individuals/get-transcript

and help

to file.

Foxconn

coned WI into $4.1 BILLION subsidy: now orders down but taxpayers billed.

Miracle:

Where is the miracle

that stops mass

killings? More crazy people or mass destruction weapons?

20

million more of us have health insurance than in 2010! 28.5 million still not

covered. We can do better: All the children in New England are insured.

We

fell 84 floors in broken elevator -- lived to tell the tale: Grace of God?

1 good cable?

“Mick

and I live off of this fire between us” New rule: work

past age 75 for a grand life.

IAN

41 Watchung Plaza,

B242

973.746.2014

Alerts

{kind=link}